Fact: there are many online cash lenders available in the market. Tala Philippines, Moola Lending, and Loan Ranger may be dominating the market, but there is a newcomer these days and people are also raving about it.

Who is this newcomer? It’s Cashalo.

Is it safe? Is it worth applying for? Does it charge high interest rate? How’s the customer service?

Don’t worry. These questions will be answered, so make sure to stick around and find out what customers have to say about Cashalo.

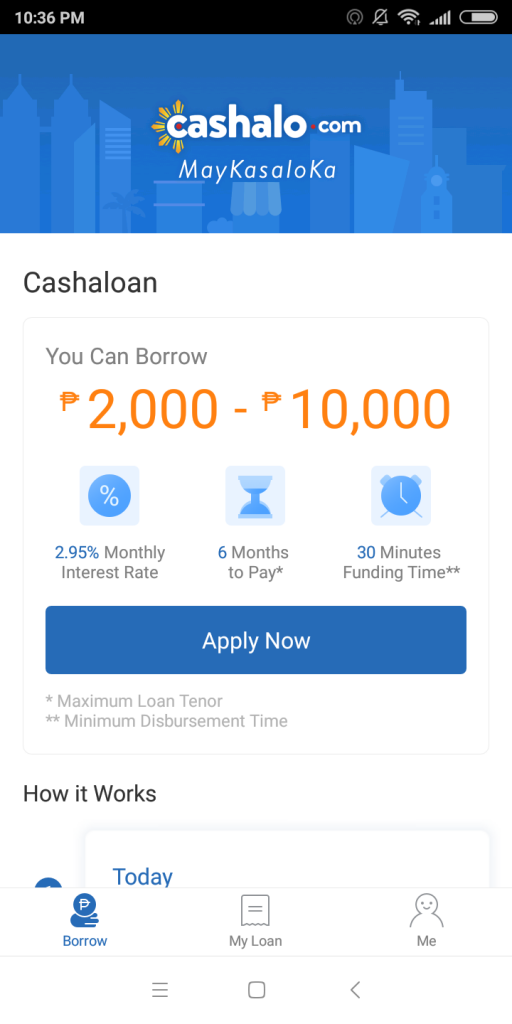

Interest Rate

Most customers who borrowed from Cashalo are in unison in saying that Cashalo has low, affordable interest rate at 3.95 percent. In fact, Cashalo’s interest rate are commended by its customers as compared to the rates offered by other online cash lenders. This is the reason why the customers interviewed took a risk and tried Cashalo.

Loan Processing

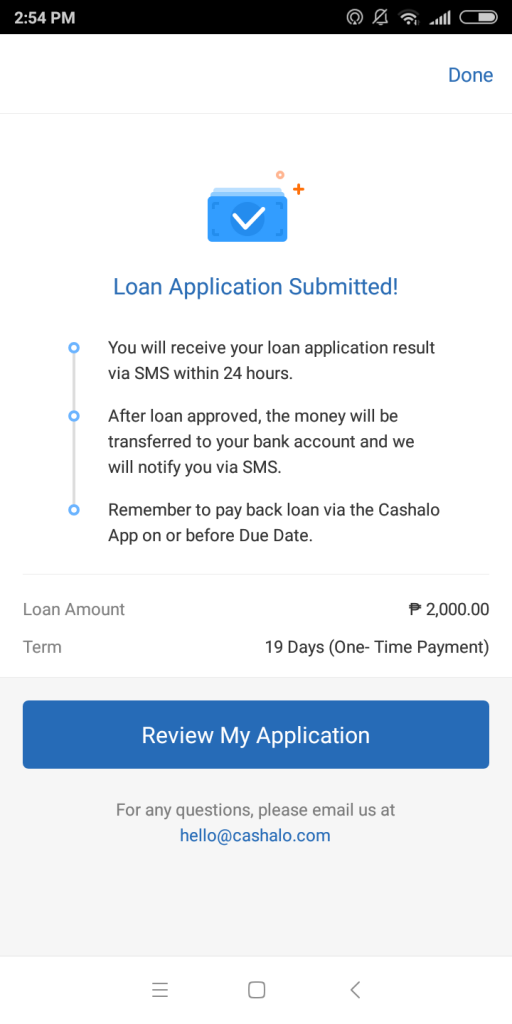

Customers have different experiences. Some say that their loan application was approved within 24 hours from the time they submitted their loan application. They got a call from Cashalo representatives for an interview to verify the details indicated in their loan application. After a few hours, the loan amount was credited to their account.

On the other hand, there are customers who experienced delay in the processing of their loan application. One customer shared that it took two days before the amount was credited to her bank account while another said that her loan application was approved after 24 hours.

Nonetheless, some of the customers interviewed said that while others experienced fast approval, there are many others who got rejected instantly. One app user said that her loan application was rejected less than a minute after she submitted her application.

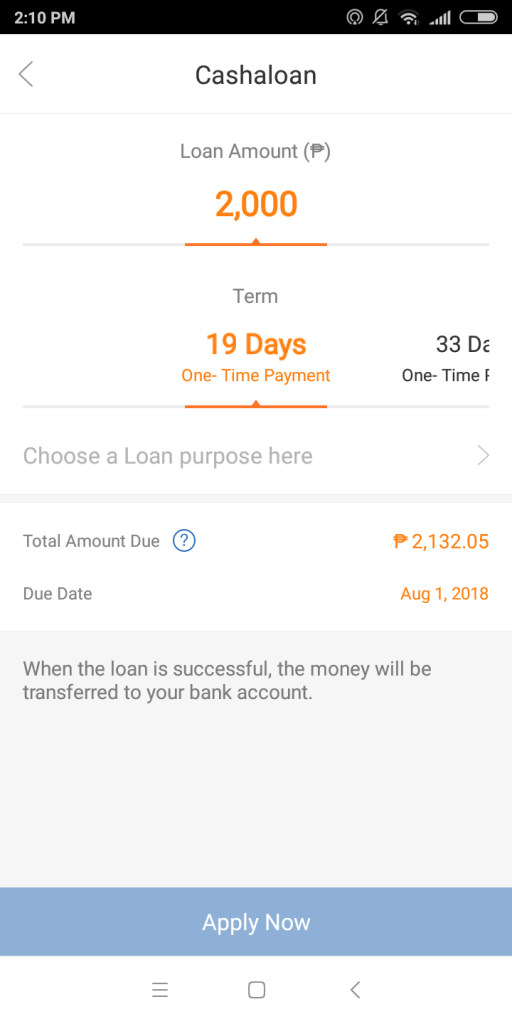

Loan Repayment

According to the customers interviewed, Cashalo’s loan repayment scheme is easy and straightforward compared to other online cash lenders they tried. Most of them paid over-the-counter through DragonPay.

Nonetheless, many of them said that they hoped Cashalo will introduce other payment schemes to make loan repayment easier and more convenient.

On Applying for a Succeeding Loan

This is another concern for most of the customers interviewed. According to them, although they paid for their first loan on time (some in advance), they had a problem applying for a second one. They echoed that paying on time and in full won’t automatically guarantee approval for succeeding loan applications.

Customer Service

This is another aspect that is commended by many customers interviewed. Most of them had good experience when it comes to Customer Service, saying that the staff who contacted them are nice and respectful.

Unfortunately, there were others who didn’t have a pleasant experience dealing with Cashalo’s customer service. They said that when making inquiries, follow-up, or clarifications regarding their loan, they rarely get a reply from Cashalo despite repeated messages. When it comes to following up payments, Cashalo representatives are so quick in sending them messages nonstop.

Overall, Cashalo’s low interest rate compared to other online cash lenders is its main selling point. Fast approval is also among its strongest feature, but it is best to lower your expectations since processing time varies per borrower. Still, try downloading the Cashalo app now to give it a try and see for yourself.

Recent Comments